Feed RSS

Feed RSS

Nice article from CB Insights.

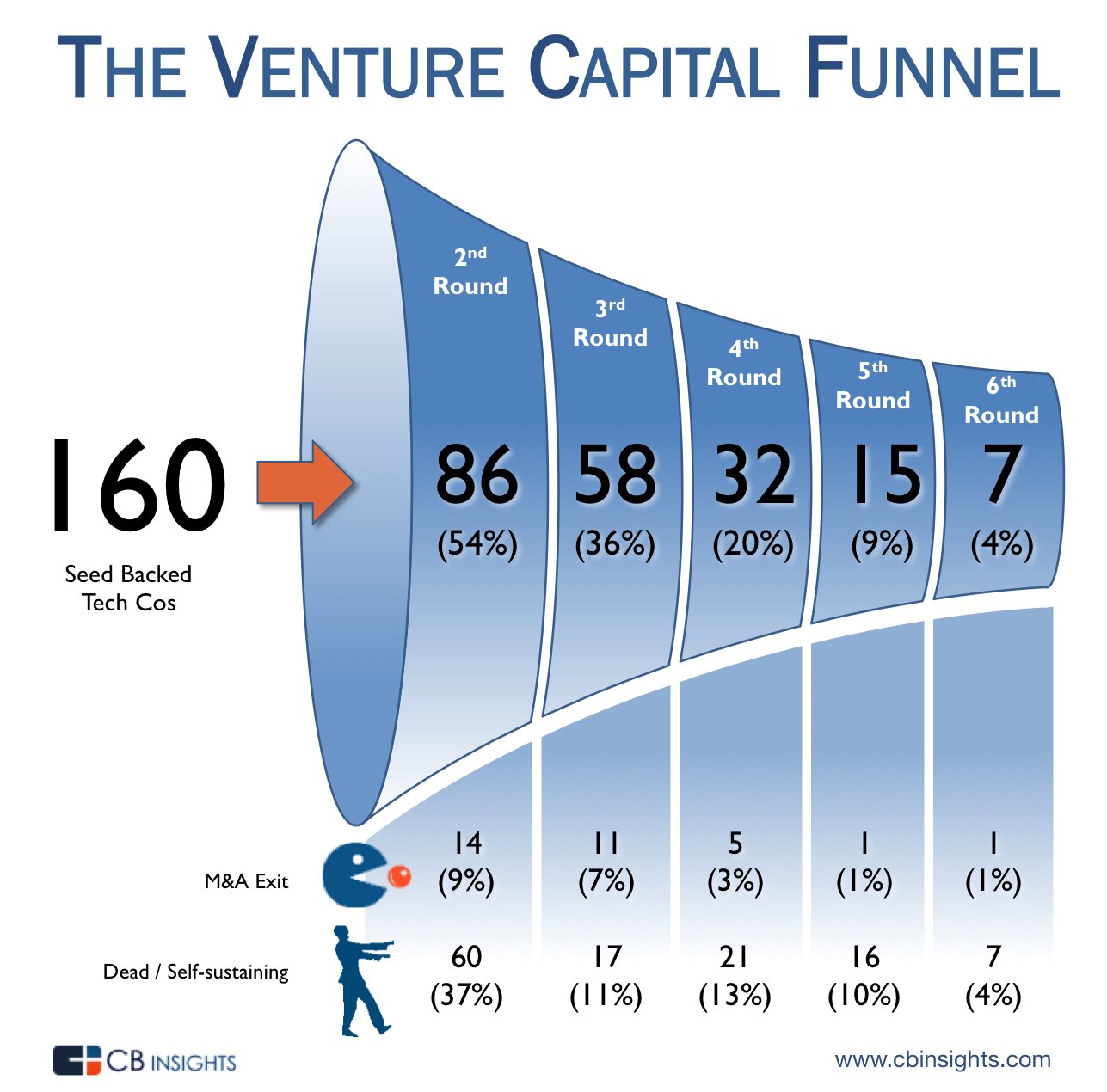

Once you take venture capital, what can you expect? Below is what the data says life will look like.

But first, some notes (based on initial comments & questions):

- This analysis uses the 2009 vintage of seed VC-backed tech companies. This is a sufficiently mature cohort of companies for us to conduct this analysis on.

- It only includes seed financings that involve a venture capital firm. Companies receiving early backing from angels, incubators, etc, while tracked by CB Insights, are not included in this brief.

- Seed VC deals were on the whole less prominent in 2009. They’ve risen in popularity in the last few years with the explosion of micro-VCs and multi-stage funds doing seed deals

Here’s some facts:

- After an initial seed round, 54% companies raise a 2nd round of funding.

- 9% raise a 5th round of financing — Interestingly, on average, it take 5 rounds of funding to get to the elusive billion dollar valuation

- 21% see an exit via M&A

- 75% of companies are either dead, the walking dead (bad outcomes) or became self-sustaining (a potentially good outcome for the company but prob not good for their VC backers). It is hard to know the breakdown for these companies as funding announcements get a significant amount of fanfare but cash flow positivity or profitability do not. Death of companies generally happens quietly in the middle of the night (although increasingly, startups are willing to share their failure post-mortems)

How hard is it for seed-backed startups to raise four follow-on rounds? By the fourth follow-on, just 20% of the initial group of tech startups are left in the funnel.

The odds of having enough gained enough traction to make it to a fifth follow-on financing were just 9%. By this mark, 19% of the startups had been acquired or acqui-hired. That fewer than 10% of the seed VC-backed tech startups in 2009 were able to make it to five, let alone six, rounds of follow-on funding speaks to the immense difficulty of continuously raising financing as a venture-backed startup.